Read on Twitter

Read on Twitter

Thread. Many are discussing student debt forgiveness. (e.g. @MattBruenig) One question is if forgiveness primarily benefits higher income households.

tldr; Survey of Consumer Finances is a key data source for determining who holds student debt, but is not well suited to the task.

tldr; Survey of Consumer Finances is a key data source for determining who holds student debt, but is not well suited to the task.

Reports describe SCF as a survey of "families." That is actually not quite right. It is a survey of a subset of households. Each household contains a "Primary Economic Unit" (PEU) that consists of the "economically dominant single person or couple" and their dependents.

that consists of the \"economically dominant single person or couple\" and their dependents.")

The survey is addressed to this PEU subset and captures all their assets and debt.

*But* many people, particularly younger adults, are not part of a PEU and have no opportunity to be interviewed. These include adult children, roommates, those in institutional housing, etc.

*But* many people, particularly younger adults, are not part of a PEU and have no opportunity to be interviewed. These include adult children, roommates, those in institutional housing, etc.

If someone wants to know the characteristics of who holds student debt, SCF can only provide an estimate of debt held by those who are part of the "economically dominant single person or couple."

Other debt holders who live with their parents or roommates are not represented.

Other debt holders who live with their parents or roommates are not represented.

This would not be a problem if debt was overwhelmingly held by "dominant" household members. We can check this issue by comparing total student debt estimated by SCF against other aggregate measures. In 2013, SCF underestimated student debt by about 30%.

https://www.federalreserve.gov/econresdata/feds/2015/files/2015086pap.pdf">https://www.federalreserve.gov/econresda...

https://www.federalreserve.gov/econresdata/feds/2015/files/2015086pap.pdf">https://www.federalreserve.gov/econresda...

Here is another analysis from the Fed making the same point about the sample and the failure of SCF to reflect all outstanding student debt.

https://www.federalreserve.gov/econresdata/notes/feds-notes/2015/how-much-student-debt-is-out-there-20150807.html">https://www.federalreserve.gov/econresda...

https://www.federalreserve.gov/econresdata/notes/feds-notes/2015/how-much-student-debt-is-out-there-20150807.html">https://www.federalreserve.gov/econresda...

A 2014 paper asks, "Are SCF young adults representative of all young adults?" They "compare the SCF data with those in sources that are representative at the individual (rather than household) level."

*They find young people in SCF have higher income.*

https://files.stlouisfed.org/files/htdocs/publications/review/2014/q4/dettling.pdf">https://files.stlouisfed.org/files/htd...

level.\"*They find young people in SCF have higher income.* https://files.stlouisfed.org/files/htd...")

*They find young people in SCF have higher income.*

https://files.stlouisfed.org/files/htdocs/publications/review/2014/q4/dettling.pdf">https://files.stlouisfed.org/files/htd...

New 2019 SCF data indicate that total outstanding student debt is $1.1 trillion. However, the Fed& #39;s G.19 data report $1.6 trillion.

https://abs.twimg.com/emoji/v2/... draggable="false" alt="🚨" title="Polizeiautos mit drehendem Licht" aria-label="Emoji: Polizeiautos mit drehendem Licht">That means about $500 billion or 31% of all student debt is not accounted for by the "dominant" household members included in the 2019 SCF.

https://abs.twimg.com/emoji/v2/... draggable="false" alt="🚨" title="Polizeiautos mit drehendem Licht" aria-label="Emoji: Polizeiautos mit drehendem Licht">That means about $500 billion or 31% of all student debt is not accounted for by the "dominant" household members included in the 2019 SCF.

Matt Bruenig wrote a good overview of this SCF measurement issue last year.

https://www.peoplespolicyproject.org/2019/06/27/low-income-people-have-more-student-debt-than-realized/">https://www.peoplespolicyproject.org/2019/06/2...

https://www.peoplespolicyproject.org/2019/06/27/low-income-people-have-more-student-debt-than-realized/">https://www.peoplespolicyproject.org/2019/06/2...

After Bruenig published this piece, Adam Looney at Brookings responded that he had "calculated exact estimates of the income distribution of student loan borrowers using administrative data from the Department of Education matched to...tax records" https://www.brookings.edu/blog/up-front/2019/06/28/who-owes-the-most-student-debt/">https://www.brookings.edu/blog/up-f...

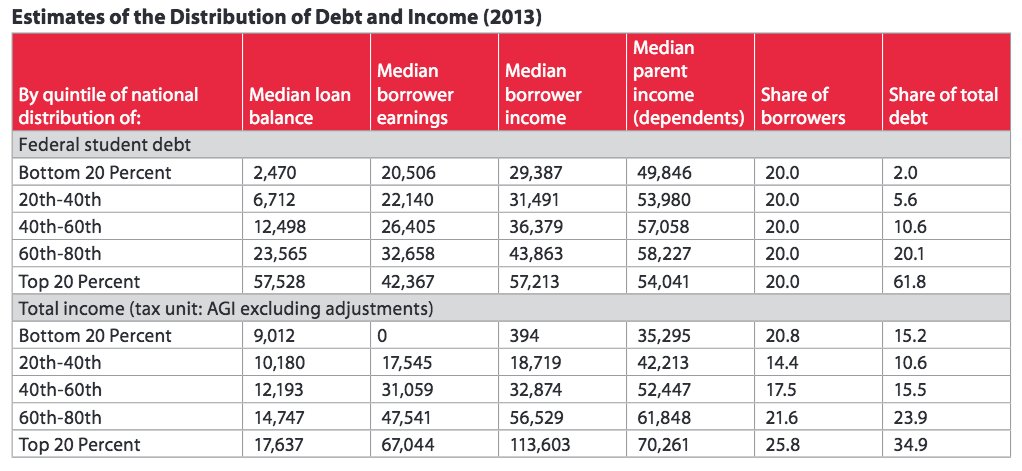

Looney compares the income distribution of student debt in the 2013 admin data to the 2016 SCF data. The pattern is generally consistent, but the income quintiles in the admin data are different from SCF.

Median wage in the bottom quintile is $394 in admin data vs $16k in SCF.

Median wage in the bottom quintile is $394 in admin data vs $16k in SCF.

Looney& #39;s data suggest even if student loan debt is held disproportionately by higher income people, a large share of that debt is still held by people with low income.

However, the data is also seven years old, so things may have changed since then.

However, the data is also seven years old, so things may have changed since then.

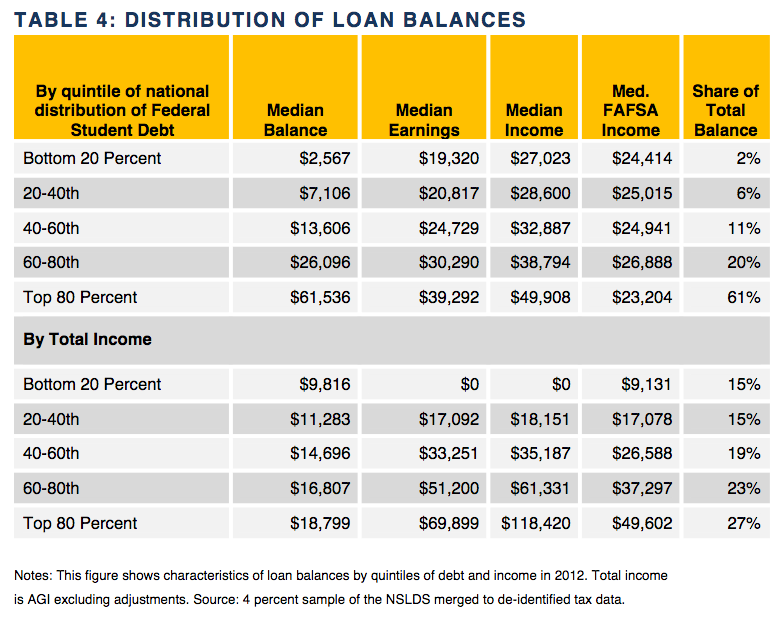

Another issue is that there are two similar reports. The "exact" estimates in a 2016 report using 2013 data are quite different from a 2018 report using 2012 data.

The top income quintile holds 27% of student debt rather than 34.9.

https://siepr.stanford.edu/sites/default/files/publications/PolicyBrief-July16.pdf

https://siepr.stanford.edu/sites/def... href=" https://www.brookings.edu/wp-content/uploads/2018/02/es_20180216_looneylargebalances.pdf">https://www.brookings.edu/wp-conten...

The top income quintile holds 27% of student debt rather than 34.9.

https://siepr.stanford.edu/sites/default/files/publications/PolicyBrief-July16.pdf

https://www.brookings.edu/wp-conten..." title="Another issue is that there are two similar reports. The "exact" estimates in a 2016 report using 2013 data are quite different from a 2018 report using 2012 data.The top income quintile holds 27% of student debt rather than 34.9. https://siepr.stanford.edu/sites/def... href=" https://www.brookings.edu/wp-content/uploads/2018/02/es_20180216_looneylargebalances.pdf">https://www.brookings.edu/wp-conten...">

https://www.brookings.edu/wp-conten..." title="Another issue is that there are two similar reports. The "exact" estimates in a 2016 report using 2013 data are quite different from a 2018 report using 2012 data.The top income quintile holds 27% of student debt rather than 34.9. https://siepr.stanford.edu/sites/def... href=" https://www.brookings.edu/wp-content/uploads/2018/02/es_20180216_looneylargebalances.pdf">https://www.brookings.edu/wp-conten...">

https://www.brookings.edu/wp-conten..." title="Another issue is that there are two similar reports. The "exact" estimates in a 2016 report using 2013 data are quite different from a 2018 report using 2012 data.The top income quintile holds 27% of student debt rather than 34.9. https://siepr.stanford.edu/sites/def... href=" https://www.brookings.edu/wp-content/uploads/2018/02/es_20180216_looneylargebalances.pdf">https://www.brookings.edu/wp-conten...">

https://www.brookings.edu/wp-conten..." title="Another issue is that there are two similar reports. The "exact" estimates in a 2016 report using 2013 data are quite different from a 2018 report using 2012 data.The top income quintile holds 27% of student debt rather than 34.9. https://siepr.stanford.edu/sites/def... href=" https://www.brookings.edu/wp-content/uploads/2018/02/es_20180216_looneylargebalances.pdf">https://www.brookings.edu/wp-conten...">

So - SCF data does not include many adults who hold as much as $500 billion in student debt. This makes it impossible to know the distribution of the debt.

2013 admin data indicate many low income people hold student debt even as the larger share is held by higher income people.

2013 admin data indicate many low income people hold student debt even as the larger share is held by higher income people.

As policymakers consider student debt forgiveness, it is important to take into consideration that we do not have a good understanding of who holds that debt. The common assumption that student debtors have good income may or may not be correct. What& #39;s needed is better data.